Alibaba is backing the development of Singapore’s tallest tower at 8 Shenton Way (SOM)

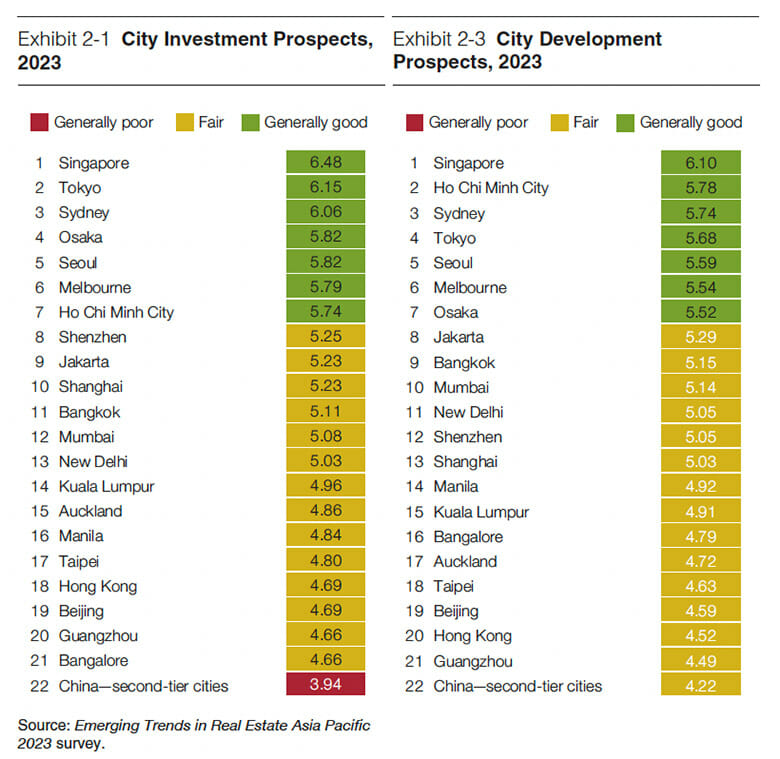

Singapore has edged out Tokyo as the most favoured Asia Pacific property investment destination in 2023, reclaiming a title it previously held two years running, according to a report released this week.

The nonprofit Urban Land Institute, which issued the Emerging Trends in Real Estate Asia Pacific 2023 report in cooperation with PwC, said Sydney held on to third place in the survey, which covers 22 metropolitan areas.

“The persistence of fragmented market conditions has enabled Singapore and Tokyo to retain their top spots as the cities with the brightest investment prospects,” said Stuart Porter, PwC’s Asia Pacific real estate tax leader.

The ULI said Singapore benefitted from the redirection of capital that might otherwise have been placed in assets in China and Hong Kong. The Lion City has also seen a significant number of businesses, including offshore asset management companies set up in the city rather than Hong Kong.

Revenue Tailwinds

One Singapore developer told the report’s authors that “headwinds on the [construction] cost side have been offset by tailwinds on the revenue side.” Singapore’s full-year office rents for 2022, for example, are projected to grow some 8 percent, according to CBRE, one of the biggest increases regionally.

The report gauged prospects for both investment and development

Tokyo’s high position represents overall positive investor sentiment toward Japan, with Osaka placing fourth in the rankings. Japan’s near-zero interest rate environment ensures lower borrowing costs and a more positive spread over the cost of debt.

While Japan has always been a draw for international capital due to its deep and liquid markets, it has appealed this year because domestic interest rates – and cap rates – have remained stable even as global rates rise sharply.

Australia’s appeal as a “go-to market for global investors” has ensured that commercial real estate volumes remained strong in 2022. Not only did Sydney place third in the report’s rankings, but Melbourne, expected to become Australia’s largest city in 2026, ranked sixth. Australia continues to be a big destination for Singaporean and Japanese capital, the report said.

New Set of Threats

ULI and PwC noted that compared with surveys from the previous two years, this year’s rankings show an “uptick in positive sentiment”, with seven regional cities scoring in the ‘generally good’ range (compared with six last year), one in the ‘generally poor’ range (compared with three last year), and overall scores higher than either the 2021 or 2022 reports.

Stuart Porter of PwC

But although Asia Pacific markets outside China appear to be recovering from the effects of coronavirus pandemic, investors say new threats include high inflation, rising interest rates, unsustainable levels of public- and private-sector debt and the possibility of global recession.

Investors have become more defensive, the report said, focusing on rent indexation, shorter lease terms that can more easily incorporate rent increases and reliable recurrent income. Accommodation – including multifamily residences, hotels, old-age homes and student housing – is one such sector.

Logistics was described as another boom area due to chronic undersupply. “Specialist asset classes such as data centres, cold storage, and life sciences, meanwhile, have “sticky” qualities as well as long index-linked leases and generally high rents,” the report said.

Big Funds Dominate

Investment has increasingly been dominated by large global funds, with less activity seen from domestic buyers. But the report noted that 2022 saw a decline in transaction volumes, with the deal count in the third quarter falling 38 percent year-on-year to $32.6 billion, the lowest recorded in the region for a decade.

China accounted for the biggest decline with a fall of 23 percent year-on-year. The highest ranked Chinese cities were Shenzhen (eighth) and Shanghai (10th).

Mainland retail assets, the report said, have “largely been relegated to the sidelines” due to concerns over potential pandemic-related shutdowns and a decline in consumer spending. Offices in core business districts suffer from oversupply issues, especially in Shanghai.

The reported noted a decentralization trend in both Shanghai and Hong Kong, with large peripheral clusters of new towers developing around Shanghai’s railway station as well as in the North Bund and Qiantan areas. “As often happens in China, growth has been so rapid that oversupply problems have arisen, though these should be digested in a period of two to three years,” according to an investor quoted in the report.

In Hong Kong, the report said, secondary commercial hubs have evolved in Kowloon East and Quarry Bay that draw back-office departments and, increasingly, professional service firms fleeing the city’s “notoriously high rents”.

In terms of real estate capital flows, China continues to be vital to manufacturers due to the depth and complexity of domestic supply chains, but the migration of new industrial capacity to other jurisdictions has accelerated in 2022 due to ongoing COVID-related travel and operational restrictions.

Indonesia, the Philippines and Vietnam have emerged as attractive investment destinations due to high rates of economic growth, emerging consumer classes, and flows of foreign direct investment into new manufacturing facilities.

Leave a Reply