Fast-growing real estate agency Lianjia has been criticised for diving into down-payment loans

China’s government has aimed a barrage of measures at creating demand for housing in the country’s lower tier cities in the last several months, and the result has been a rise in home prices of as much as 50 percent. In all the wrong places.

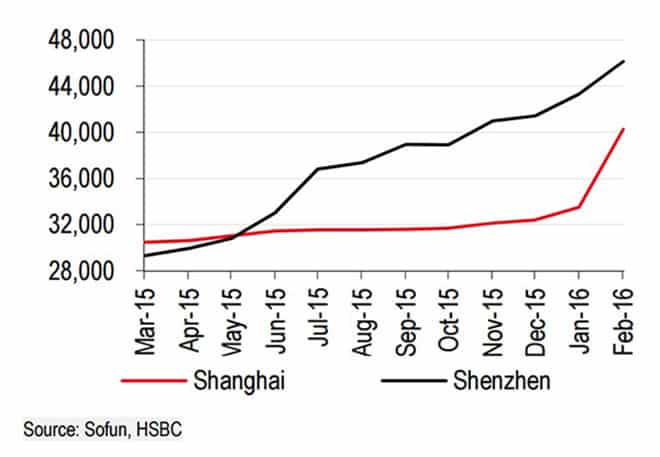

Despite carefully excluding the first tier cities of Shenzhen, Shanghai, Beijing and Guangzhou from measures aimed at rekindling mainland housing markets, prices in Shenzhen rose more than 3.6 percent last month compared to January, with Shanghai’s market not far behind with 2.9 percent month on month growth. Home prices in Shenzhen are now up by nearly 57 percent compared to the same period last year.

The government has already vowed to tamp down the real estate frenzy in first tier cities, but may find it difficult to take on the network of speculators, private lenders and fearful people looking for a place to live, that are driving the renewed bull run in China’s big city home sales.

FOMO and the Latest China Bubble

BBVA economist Le Xia is getting nervous about China’s housing market

Last year China’s stock market famously rose to record highs as the Shanghai composite index climbed to over 5166 as millions of retail investors feared missing out on an epic bull run encouraged by the government. By June the market was in trouble and it has continued to stumble downward, despite massive government bailout efforts, until it now rests at 3018 – even lower than before the craze started.

Now, many of the same investors who raced into stocks for fear of missing out on the last great opportunity – to own a home, to become a millionaire, to get married, whatever that opportunity is – are pouring their savings into the country’s first-tier city real estate markets. Investments which are seen as one of the few remaining stable opportunities in the country.

But are China’s first tier cities really as safe as houses?

There is growing evidence that the fervor for China’s first tier markets, such as Shanghai – where $1 million buys you only a 46-square metre home in Shanghai, and property values along Nanjing Road in the city’s Jing An district now average over RMB 100,000 ($15,500) per square metre – is driving many investors to skirt downpayment rules and turn to shadow lenders to speculate on the market. And these innovative financial practices are bringing new levels of risk to the market.

“I have been very nervous about this because it reminds me of the US subprime crisis,” Xia Le, chief economist for Asia at BBVA was quoted as saying in the Financial Times. “In the past, people buying houses paid using their own money but now they’re using speculative shadow finance.”

Measures Designed to Exclude the First Tier

The fever for homes in Chinese biggest cities raises questions about the effectiveness of government measures to revive the housing market, as well as about the wisdom of the country’s reliance on cheap credit to fuel growth.

First Tier Home Prices Grew By As Much as 50% in the Last Year

With an eye on reviving a property sector where growth in new investment slid to just one percent in 2015, China’s government has cut down payment rates three times in the last year, with the most recent round – in February – lowering the minimum mortgage down-payment for first-home purchases to 20 percent from 25 percent and to 30 percent from 40 percent for second homes.

However, China’s first tier cities of Shenzhen, Shanghai, Beijing and Guangzhou were all explicitly excluded from these relaxation of home purchase controls.

Also last month, the government lowered transaction taxes on home sales. But the first tier cities were once again excluded from these measures.

Despite government attempts to work around first tier markets in stimulating the real estate industry, the average price of a new home in Shanghai jumped to a record RMB 35,911 per square meter ($509 per square foot) last month, according to Soufun data. In Shenzhen rates have risen to the equivalent of $659 per square foot.

Much of the fuel for new home-buying appears to come from the government’s reduction of interest rates and increases to the money supply in recent months.

After the PBOC’s six rounds of rate cuts since 2014, and injections of liquidity into the banking system, medium and long term bank loans to households – mostly residential mortgage loans – grew by RMB 478.3 billion ($73.5 billion) in January, according to the central bank.

Agencies Guide Buyers Around Down Payment Laws

Another source of money pouring into the property sector is some business innovation by the country’s loosely regulated real estate agencies. Some residential realtors have begun branching out into financing to help drive more transactions and provide new sources of revenue.

Official media has singled out Lianjia, a Beijing-based agency that has recently used acquisitions of rivals in Shanghai and other cities to grow its network, for providing downpayment loans for homebuyers who can’t meet the government minimum requirements for buying a home.

The agency loaned an estimated RMB 4.5 billion to clients seeking downpayment loans at rates, that after adding in service charges, reached as high as 24 percent. The agency, along with some of its rivals in Beijing, has since been forced to curtail its money-lending business.

Lianjia, which has also reportedly been coaching homesellers to boost asking prices, raises money for the downpayment loans through online P2P debt products. The real estate broker then uses the funds to allow homebuyers to take on more leverage than a traditional bank would allow, and makes it easier for less qualified buyers to take on debt.

Homeowners Aren’t Over-leveraged And Other Ancient Legends

HSBC head of China research Zhiming Zhang

The rush of money into the property sector, especially from non-traditional and lightly regulated sectors such as the peer-to-peer lending industry undermines the low levels of leverage that have long been a major source of stability in the country’s housing market.

“The credit growth has fed into rising asset inflation, notably in property prices and especially those of first tier cities,” HSBC analyst Zhiming Zhang said in recent note to clients earlier this month. “There are signs that speculative forces are at play, aided by the credit boom, a flourishing shadow banking sector and P2P (person-to-person) financing.”

Aided by the growth of online financial platforms, China’s peer-to-peer lending industry handled RMB 982 billion ($149 billion) in loans during 2015, almost four times the 2014 total. And the government first began regulating the fast growing money lenders in December.

As many as 15 large peer-to-peer lenders have been granting unsecured mortgage loans to home buyers in Shenzhen, Shanghai and Beijing, according to the FT, although the government is now moving to clamp down on the practice in the capital.

Even if the government forbids provision of loans explicitly for down payments, it has little control over what consumers do with the funds, once peer-to-peer loans have been made. There are added dangers should borrowers take on loans from multiple lenders to purchase several properties in the booming market.

Government Vows to Crack Down

In reaction to the rapidly rising home prices in Shenzhen and Shanghai, government regulators have vowed to take action to curb the buying frenzy in general, and to end down payment loans specifically.

Although giving loans for downpayments has always been illegal for traditional lenders, new rules being drafted are said to forbid developers, real estate agencies and peer to peer networks from providing this type of funding.

However, details on how the government would police China’s shadow bank lending practices, and the highly entrepreneurial P2P lending sector, have not yet been disclosed. The government has indicated that the central bank and the China Banking Regulatory Commission will ask commercial banks to reject loans to applicants who admit that they had used illegal sources to make down payments.

Crowdfunding Sites Creating DIY MBS

Making enforcement more challenging for government regulators is the rise of crowd-funding sites, which are naturally turning their attention to the profit opportunities in booming big city housing markets.

A site named pinfangwang.com.cn allows China’s netizens to invest as little as RMB1,000 ($155) to own a share in a housing asset. The site is one of a number of online products that have essentially begun assembling mortgage-backed securities on the Chinese Internet, without giving buyers a clear view of the underlying assets.

For anyone who is a fan of US movies, the scenario combining China’s loosely regulated private lending industry, with a booming housing market and the anonymity of the Internet may sound like a scary mashup of The Big Short, the Social Network, and Nightmare on Elm Street.

Leave a Reply